THE ADVANTAGES OF HAVING LIFE INSURANCE:

1) Life insurance contracts under French law offer tax and inheritance advantages. In addition to the Euro fund offered by your insurer, you have the option of subscribing to investment funds within your contract, generally consisting of bonds, stocks, and sometimes real estate.

2) In addition to tax and inheritance advantages, life insurance contracts under Luxembourg law offer optimal security, diversity and flexibility.

3) Luxembourg is tax neutral, that is to say that the subscriber of the life insurance contract will pay taxes in his country of residence and not in Luxembourg. For example, if you live in France, you will be subject to French taxation regarding your life insurance you contracted in Luxembourg.

4) The capitalization of income is not taxable if they are not redeemed. Arbitrations, i.e. purchases and sales of assets within the fund are not taxed. Indeed, if the manager carries out arbitrations and orders between the fund sub-funds, no taxes will be applied.

5) For a French resident, the tax rates are decreasing from the 5th year, with a tax optimization after the 8th year.

6) The contract is subject to the French Wealth Tax but only at its nominal value, capitalized income is not taken into account.

7) The double taxation treaties signed between Luxembourg and other countries prevent contracts from being double taxed, which offers another significant advantage.

8) Life insurance under Luxembourg law offers advantages at the time of inheritance. The policyholder, that is to say the one who subscribes, is free to choose the beneficiaries and he can set premiums for them. At the time of the death of the policyholder, the beneficiaries are entitled to a reduction according to their relatives with the deceased, and they will be subject to an advantageous taxation on the amounts.

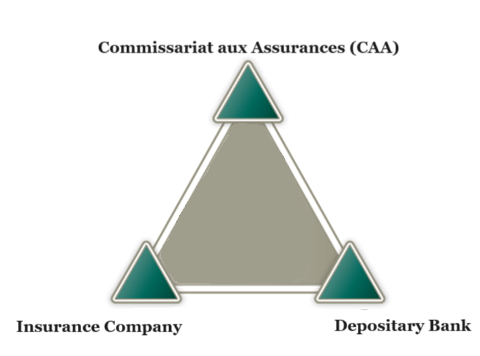

9) The policyholders and their interests are protected in the event of failure of the insurance company and the depositary bank, below the security triangle. Indeed, during the 2008 crisis, four Irish partner banks went bankrupt, so the insurer transferred their clients’ securities to another bank.

10) The underlying assets held by the client are confidential, no one can know what is in the fund, only the number of units is known. In addition, the contract is protected, it cannot be seized by a third party except during legal proceedings,

11) The life insurance contract can be used as collateral when making a bank loan,

12) From a minimum investment of 250,000 euros, the contract can contain a wide range of underlyings such as stocks, bonds, FX, options/futures, unquoted securities and real estate,

13) It is also very flexible, the subscriber can integrate different currencies, and he has the choice of the Manager Portfolio,

14) Life insurance companies in Luxembourg seek to make returns above the market, such as results above a CAC 40 type index, otherwise, clients will have little interest in subscribing to it,

15) Finally, the choice of Luxembourg is also another advantage because it is a politically and economically stable country.

WHAT WE ARE NOT TELLING YOU, AND WHY YOU SHOUDN’T HAVE IT ANYMORE:

1) Life insurance has been on the rise for several decades. Indeed, it is an excellent way to optimize your taxation while obtaining attractive returns. However, I really think that this time is over,

2) In France, the rates of return on Euro funds have only fallen for 20 years,

3) For French resident: the French Sate will most certainly end up tackling the advantageous taxation of life insurance to bail out the public debt which has become out of control,

4) Also when the next financial crisis arrives, you will suffer significant losses on your contracts, or even a total loss in the event of bankruptcy of your insurer, which it should be emphasized are already in great financial difficulty for some (especially in France) because of the rise in interest rates decided by the central bank which led to a crash in bond markets,

5) As for contracts governed by Luxembourg law, the law obliges to respect ratios on the types of assets in each portfolio (a certain percentage for bonds, shares, etc.). This means that the manager must keep a minimum amount of bonds in the portfolio and that in theory he cannot convert everything into cash,

6) Even if Luxembourg is a world-renowned financial center, the quality of management in insurance companies has decreased due to shareholder pressure to always get more profit, so the number of employees per team is reduced, as is the cost of IT systems,

7) Concerning the Sapin 2 Act on French life insurance contracts:

French life insurance contracts, composed on a large scale of bonds, i.e. debt, are subject, in France, to the Sapin 2 Act (voted in 2016 by the Minister of economy Michel Sapin), which authorizes the blocking of purchases, even partial. This law was enacted to curb insurer bankruptcy in the event of panic in the stock markets.

→ Thus, the conventional euro fund that makes up your life insurance can bear major losses on the bond market without you being able to redeem the shares from your insurer, thereby increasing the risk of a total loss of your investment.

Written on September 20, 2024

Similar Posts

From France to North Cape in a retro car (video) – TRAVEL

In total, 11,000 kilometers crossed through 11 countries in a Renault 4L during the summer of 2017. Published on April 13, 2023

Montenegro: the pearl of the Balkans – EXPATRIATION/TRAVEL

Montenegro, a picturesque country on the Adriatic coast, nestled in the heart of the Balkans, boasts not only stunning landscapes, rich cultural heritage,…

Tired of high taxes in the UK? EXPATRIATION

Tired of high taxes in the UK? Relocation to the United Arab Emirates is the ideal solution! We offer a full range of…

Increase your physical and intellectual abilities (part 2) – HEALTH

To further increase your physical and intellectual abilities, you will imperatively have to develop your spirituality. These three poles work in synergy. When…

In search of the keys to the Universe – ESOTERICISM/SPIRITUALITY

After leaving London at the beginning of autumn 2016, I flew to Kazakhstan in particular to visit a friend in Astana. This trip,…

Increase your physical and intellectual abilities – HEALTH

Our body is the instrument that allows us to flourish fully, in harmony with the environment that surrounds us. The quality of our…